Originally published in Spanish on Energy Report. Estimated read time: 14 minutes.

Argentina’s lithium sector has a new ten-year roadmap.

According to public and private estimates obtained by the Herald’s sister publication, Energy Report, over the coming ten years the country’s “atomic number 3” industry is expected to triple in size, surpassing a total installed production capacity of 650,000 tonnes of lithium carbonate equivalent (LCE).

If just over half of that total were processed and exported, Argentina would climb into the world’s top three lithium producers, competing directly with first-placed Australia, second-placed Chile, and third-placed China.

But if, within the next decade, the eight planned processing plants come online — alongside the seven already in operation — then the country could become the world’s single largest producer of lithium for the global energy transition.

Data from the U.S. Geological Survey (USGS) show that in 2023, global demand for lithium carbonate equivalent reached 920,000 tonnes, with 84% of that destined for the battery industry. Demand rose to 1.27 million tonnes in 2024, and is expected to reach 1.34 million tonnes this year.

According to projections from S&P and Benchmark Mineral Intelligence, by 2035 global demand for lithium could reach between 3.3 and 3.8 million tonnes of LCE — triple the 2024 level, representing growth of more than 230%. That’s precisely where Argentina’s opportunity lies.

The USGS also reported that measured and indicated lithium resources worldwide total 115 million tonnes. Argentina leads this global ranking, with just over 23 million tonnes, ahead of Bolivia (23 million), Chile (11 million), Australia (8.9 million), and China (6.8 million). Clearly, the country has significant room for growth.

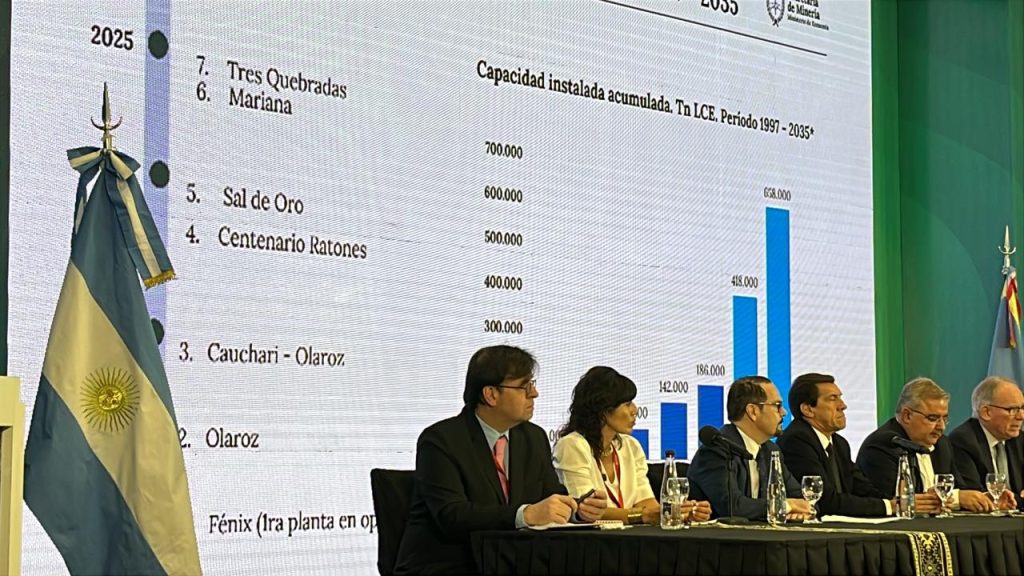

This potential exponential leap was underscored by Luis Lucero, Argentina’s National Secretary of Mining, during the opening ceremony of the recent Lithium in South America Seminar, organized by Panorama Minero in Catamarca. Addressing an audience of governors, business leaders, experts, and suppliers, Lucero displayed a bar chart that sparked enthusiasm among the more than 1,000 attendees.

“The growth achieved over the past ten years has been exceptional,” Lucero said, noting that Argentina’s installed production capacity has risen from 35,500 tonnes of LCE per year to 186,000 tonnes annually.

“Argentina is today an international player of the highest relevance in the global lithium market, and we can only hope and work for its importance to keep growing,” he concluded.

Record output for Argentina

Today, the world’s largest producer is Australia, which accounts for 37% of total production. Chile follows with 23%. This year, Chile expects to reach a cumulative lithium output of 305,000 tonnes of LCE, according to projections by Cochilco, the Chilean state mining agency — a significant increase from the 285,000 tonnes recorded in 2024. Argentina, with seven operating plants, is expected to end 2025 with record figures.

A private report based on company data, which Energy Report has seen, indicated that in the first half of 2025, production reached 51,400 tonnes of LCE, equivalent to 57% utilization of installed capacity. For the second half of the year, the report expects ramp-up processes at the newest plants — Tres Quebradas, Mariana, Sal de Oro, and Centenario Ratones — to continue, boosting production performance by 27% and closing the year with around 115,000 tonnes of LCE produced. The most optimistic voices at the seminar speak of reaching 140,000 tonnes. Time will tell.

What is certain is that in the first eight months of 2025 (through August), lithium exports totaled US$494 million, marking year-on-year growth of 32% in value and 56% in volume. This figure represents 14% of total mining exports, making lithium the country’s second most-exported mineral. But the key question remains: how much investment is needed for Argentina to become one of the world’s top lithium producers?

Over the past ten years, lithium mining companies have invested US$7.6 billion to bring production capacity to 183,700 tonnes of LCE today. According to private-sector estimates, launching 17 of the 30 registered new projects would require an additional US$12.8 billion in investment — enough to raise Argentina’s productive capacity to 580,000 tonnes of LCE. In Catamarca, Lucero spoke of reaching 2035 with 15 operating plants and about 658,000 tonnes of LCE capacity. One way or another, the challenge is immense — and there is still much work ahead.

Hopping the first hurdles

The first hurdles to overcome are international competition and weak prices. Today, China controls global lithium purchases and, with that, sets the market price. Electrification is advancing rapidly, but goes through periods of slowdown. Lithium is not a traditional commodity, and its price fluctuates according to the market. The thermometer of international value depends largely on China’s production and consumption of electric vehicles and other electric products, but also on global supply.

International prices are set through purchase agreements between producers and buyers, though these are often kept under commercial secrecy. It is known that, on average, a tonne of lithium currently sells for around US$10,000 dollars, with delivery contracts extending up to two years. Some deals, however, are signed for just above US$8,000 per tonne.

In late 2023, global shipments were contracted for up to US$83,000 per tonne. In Argentina, prices never exceeded US$55,000 per tonne, with a 4% federal export tax that, for now, remains unchanged. The issue was barely mentioned in the country’s northern provinces, as no one wanted to stir tension. Naturally, mining companies argue that removing those export taxes would be a positive gesture toward a sector seeking to expand and increase output, at a time when the international situation grows more challenging by the day.

As several foreign analysts warned during the Catamarca event, the global lithium market is currently facing a mix of limited but rising demand and an abundant supply. Federico Gay, principal analyst at Benchmark Mineral Intelligence, noted that in 2025 alone, lithium demand will rise by 24% compared to last year, with 65% of that demand coming from electric vehicles. He added that lithium’s annual growth projection of 15% is unmatched by any other mineral.

Gay also pointed out that this year an additional 100,000 tonnes of lithium will enter the market from Africa, and global production will rise by 200,000 tonnes compared to last year. This will lead to oversupply. Initially, that will compensate for the higher prices that followed the temporary suspension of the Lianxiawo mine in China, operated by battery giant CATL, but prices have since tumbled again after the announcement of what is claimed to be the world’s largest lithium reserve, surpassing even Argentina’s, along with other recent discoveries.

A massive lithium discovery in Germany

In late September, the company Neptune Energy announced the discovery of 43 million tonnes of lithium in Germany’s Altmark region, in Saxony-Anhalt. According to evaluations by the firm Sproule ERCE, this represents one of the largest reserves on the planet and could reshape lithium supply dynamics in Europe — which has so far been a tempting market for the “lithium triangle” countries of Argentina, Bolivia and Chile.

Initial company estimates suggest that the Altmark region could hold up to 70 million tonnes of lithium carbonate, enough to extract 25,000 tonnes annually — sufficient to manufacture batteries for around half a million electric vehicles each year. The world keeps turning, research and exploration never stop, and the external threat is significant. That was the sentiment voiced in Catamarca.

In this context, Argentina faces two additional challenges that complement the struggle against international competition. First, the federal government and the nine mining provinces must find a definitive resolution to the Glacier Law and the Wetlands Law, through either the Supreme Court or Congress. Second, the country urgently needs a comprehensive upgrade of its energy infrastructure and its road and rail logistics systems to expand exports.

If these two challenges are resolved by 2035, Argentina could transform mining into its third-largest export sector, nearly on par with agriculture and hydrocarbons. The figure of US$30 billion a year is being floated. Mining, they say, is the third engine of the airplane that will finally make Argentina take off. (The fourth is the knowledge economy, but that’s another story.)

Environmental protection: an open question

Regulating Argentina’s Glacier Law is crucial for advancing major copper projects, while clarifying the scope of the Wetlands Law is equally essential for operations in the salt flats of the Puna, where most of the country’s lithium lies. The Supreme Court has already urged national and provincial representatives to reach agreements on managing periglacial zones and applying the National Glacier Inventory. Far from rejecting this instrument, the mining sector values it.

Companies need certainty that the Glacier Law, and its complementary regulations, will allow mining in the Andes. They are unwilling to invest the millions of dollars that the RIGI large investment regime seeks to attract without this legal protection. Delegates at the Catamarca event voiced fears that a provincial judge could halt any project with a simple ruling, especially copper ventures requiring investments ranging from US$2.7 billion to US$15 billion.

You may also be interested in: RIGI: understanding Argentina’s new large investment regime

A similar disruption could occur with the Wetlands Law and lithium projects. The Wetlands Law seeks to establish minimum standards for protecting ecosystems, including salt flats. It has been debated in Congress for a decade and the Senate has approved it twice. However, it has yet to be made law. Companies see it as a potential threat to mining development.

The national government intends to amend the Glacier Law by decree to expand economic activity in periglacial areas, after which provincial legislatures would adopt the decree as their own. The Ministry of Deregulation is tasked with drafting this decree, which would then be validated by the Economy Ministry.

However, the mining sector would prefer to shield projects via a national law, passed by Congress, which would leave no room for ambiguity. This would require post-election political coordination across parties and mining provinces, with governors and ruling-party legislators building a solid majority in the name of production, employment, and foreign currency generation.

To win over skeptical or uninformed lawmakers, companies and unions are willing to bring experts, scientists, researchers, and workers to committee meetings to present information, correct misconceptions, and dispel myths about mining.

A third path for the Glacier Law would be intervention by the Supreme Court, bringing all stakeholders together, fostering an agreement among the nation, provinces, and those who feel affected, and issuing a unanimous ruling — thus insulating projects from future legal challenges. But for now, no one envisions the justices assuming such a central role or broaching the debate.

Clean energy, roads, and a mining railway

The third challenge for Argentina’s lithium sector is expanding energy infrastructure and developing a new export logistics network. A high-voltage transmission line in the Puna, supplying clean, renewable energy to processing plants, camps, and local communities, is considered essential. After that, progress will be needed on intermediate transformer stations and connections to lithium projects. One of the two industry proposals has already received approval from the International Finance Corporation (IFC), part of the World Bank Group, which promotes economic development in emerging countries through private-sector growth. Further news from the IFC is expected soon.

To address logistics, a comprehensive report was recently presented at the Federal Investment Council (CFI), offering precise guidelines to propel Argentine mining. Titled “Mining Logistics Plan,” it is part of the Federal Logistics Strategy, developed by Argentine experts of international standing. For now, the report remains confidential, but it will be unveiled prominently at PDAC 2026 in Toronto, Canada.

At the seminar, it was noted that if mining aligns with the privatization of the Belgrano Cargas railway, current freight capacity of three million tonnes could be doubled. This would lower operating costs, accelerate exports, and reduce environmental impact, among other benefits.

Before year’s end, branch-by-branch bidding will open. The state-owned company — set to disappear once the railway is privatized — has urged mining firms to participate as part of an investor pool to take charge of necessary segments. The pre-agreement to boost Belgrano grain exports with agribusiness firms Bunge, Cargill, ACA, AGD, and Louis Dreyfus is cited as a model. Will mining companies consider getting involved? Award decisions are slated for March 2026, and time is limited.

Water, lithium, and efficiency

The lithium sector also faces a production efficiency challenge. Extracting lithium from impure brine involves solar evaporation to concentrate lithium, followed by a purification, filtration, and washing process.

Some projects use four tonnes of chemical inputs for every tonne of lithium carbonate or hydroxide produced. Others require up to seven tonnes of chemicals per tonne produced, raising logistical costs.

Then there’s exploration, drilling, and proper field planning. Experts at the seminar stressed that the most efficient scenario is securing the best possible well, for the longest possible time, with optimal chemistry and hydraulics — technology balanced with water management.

Much is said about water and lithium, but little is known about the demanding work involved in geophysical and scientific studies to design proper use of freshwater for industry and brine for production. It is worth noting, for example, that brine used for lithium extraction is not suitable for human, animal, or agricultural use and is reinjected into original reservoirs after processing.

The water footprint of beef is 16 cubic meters per kilo. That figure is 2.5 cubic meters per kilo of soy, and just 0.6 cubic meters per kilo of lithium, according to figures shared during the Catamarca seminar.

Beyond the much-discussed Direct Lithium Extraction (DLE) methods used in many Argentine projects, the real efficiency dilemma is known as the “production cap.” This refers to the tonnage limits of processing plants themselves, which can only expand through additional investment and construction, since the resource remains in the same well. Thus, Argentina’s lithium potential also hinges on future expansions (those 17 planned new plants).

RIGI analysts must consider this, since they might wrongly classify projects as already operational when the goal is to build on existing capacity. That is precisely what companies are aiming for.

Lithium projects on the horizon

Private data indicate Argentina is entering a new expansion phase in its lithium industry, with over 30 registered projects and a development timeline stretching to 2033. “Lithium is the next Vaca Muerta — we must be patient,” said the CEO of the country’s leading lithium miner.

Between 2026 and 2027, attention will focus on launching and expanding key operations. In Salta, Sal de Oro (Phase 2) is set to be a near-term milestone, while in Catamarca, Sal de Vida (Phase 1), Fénix (Phase 1B), and HMW (Phase 1) will advance — three strategic projects reinforcing the province’s role within the lithium triangle.

From 2028 to 2029, development will accelerate with the start of Portezuelo Pastos Grandes–PPG (Phase 1) and later Phases 2 and 3 of that project, also in Salta. At the same time, Catamarca will add HMW Phase 2, maintaining a growth trajectory toward globally competitive production.

Between 2030 and 2033, a new wave of large-scale developments is expected. These include Kachi, HMW (Phase 3), Candelas, Fénix (Phase 2), Sal de Vida (Phase 2), and HM South, all in Catamarca. These projects, alongside new expansions, mark the maturation of a decade of investment that could bring Argentina’s installed capacity to record levels.

Additionally, around twenty initiatives remain on hold, awaiting investment decisions or environmental permits. In Jujuy, these include Cauchari, Cauchari Olaroz (Phase 2), Guayatayoc, and Salinas Grandes. In Salta, projects under review include Doncellas, Río Grande, Puna Mining, Arizaro, Rincón Oeste, and Centenario Ratones (Phase 2). In Catamarca, pending projects include Incahuasi, Salar de Antofalla, and Hombre Muerto, among others.

With this investment landscape, Argentina aims to solidify its position as a leading global lithium supplier, supporting the global energy transition. The coming years will determine which projects advance to production and which remain in exploration, amid growing international competition and sustained demand for critical minerals.