President Javier Milei’s presentation of the 2025 budget in Congress was a signal to creditors that the only guarantee is that primary surplus will be used to pay interest on Argentina’s 2025 debt.

Beyond the fact that the difficulties of the economic program have been more centered on the lack of dollars than on the fiscal front, the market celebrated that nod. Many economists believe the budget bill sent to Parliament has a similar spirit to the presidential speech. The text itself, in addition to optimism regarding macroeconomic projections, raised doubts and triggered numerous warnings about inconsistencies between the scenario outlined in the document and Argentina’s expected income and expenditure.

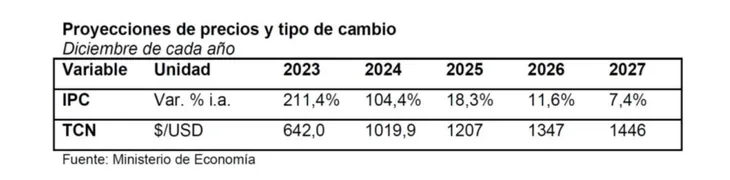

Warnings range from the forecast of 18.3% year-on-year inflation by the end of 2025 — which would imply average monthly inflation of 1.4% — to the dubious drivers behind the claim that GDP will grow by 5%. They also include the mismatch between the forecast doubling of export duties and the estimated exports and the forecast exchange rate, as well as a rebound in activity that doesn’t match the expected imports.

“The budget project is disappointing from the start,” read a report by Outlier consultancy, led by Gabriel Caamaño Gómez. “In addition to the expected excess optimism in the macroeconomic projections, the consistency of the macroeconomic scenario itself and its relation to the budget forecasts is very low, if not almost nonexistent.”

Budget and an Excess of Optimism?

Haroldo Montagu, former deputy economy minister and current chief economist at Vectorial, focused on the 18.3% monthly inflation forecast for two reasons. He told the Herald’s sister title Ámbito that “a forecast of such a low inflation rate is surprising, especially considering that August recorded 4% when less was expected and preliminary data for September indicate that it will be at least above 3%, with planned increases in tariffs and other services still pending.”

“The 104% for 2024 is already striking, the 18% for 2025 even more so,” he argued.

Outlier highlighted an apparent mistake in the project. The 18.3% accumulated inflation for next year translates to an average monthly consumer price index (CPI) of 1.4%. For 2024, the budget forecasts an accumulation of 104.4%, which would require an average monthly rate of 1.2% in the last quarter. If the figure is 3% in September, the fourth quarter would have to average less than 1%.

“The project seems to anticipate a slight acceleration in the inflation rate in 2025 compared with the end of 2024, which is contradictory,” the report emphasized. The Treasury argues that the macroeconomic scenario included in the project was prepared in June, and they now expect a somewhat higher CPI for this year.

Montagu highlighted that this inflation guideline aligns with a projection of devaluation of the official exchange rate equivalent (wholesale dollar at $1,207 by the end of 2025): “We are heading towards an appreciation that is difficult to sustain in this framework without reserves.”

Currency controls: the major omission

In the financial district, this was mostly read as a kind of tacit confirmation of the continuity of currency controls. For now, the text makes no reference to exchange controls or a unification of dollar exchange rates. “The entire issue of exchange rate liberalization is the major omission,” Outlier noted.

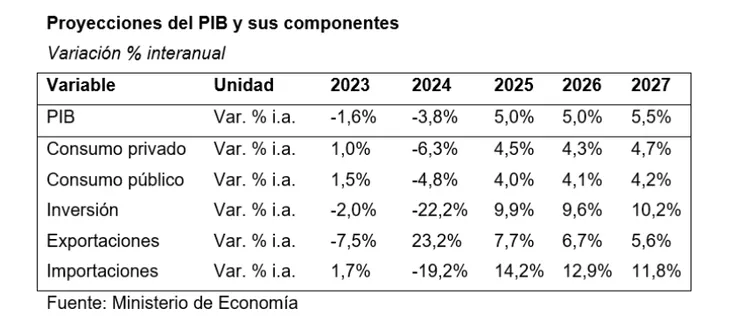

Economists also raised concerns regarding the projected 5% real GDP growth for 2025. “It is not clear what will drive this growth,” stated the Vectorial economist. The official message is that it will be driven primarily by industry and commerce, with increases of 6.2% and 6.7%, respectively, while agriculture will advance only 3.5% after an extraordinary 2024 compared to a drought-stricken 2023. “The text says that industry will drive growth, but industry has been falling by double digits year-on-year every month, so that’s unclear,” added Montagu.

As for the components of GDP, the official forecast is that private consumption will grow 4.5% (after falling 6.3% in 2024); public consumption 4% (after decreasing 4.8%); investment will rebound by 9.9% after sinking 22.2% this year; exports will increase 7.7% in volume and 9% in foreign currency terms; and imports will rise by 14.2%.

Here lies one of the main inconsistencies pointed out by economists. “A strong recovery in economic activity is projected for 2025 (+5% real), after a 3.8% drop in 2024 (this assumption is slightly more pessimistic than the local consensus). However, the balance of goods and services is almost unaffected, falling by just US$1 billion, with exported values slowing and imports accelerating. But the acceleration of imports seems too low, especially considering that a strong recovery in investment is projected for 2025,” noted Outlier.

In the same vein, Daniel Schteingart, director of productive planning at Fundar think tank, highlighted a striking detail. “The budget suggests that Argentina would have a higher GDP in 2025 than in 2023, but with imports nearly US$10 billion lower. How do they explain this, especially considering the ongoing trade liberalization? It doesn’t make sense,” he asked on X. “It occurs to me that part of it could be due to: 1) lower energy imports due to the maturing of Vaca Muerta, 2) lower soybean imports, which were high in 2023 due to the drought. Even then, the numbers still don’t add up.”

“It seems we are heading towards an import substitution industrialization regime. Full-on Peronism,” another economist quipped to Ámbito.

Will export duty revenues double?

The point that generated the greatest stir among analysts was the projected income scheme for the next year. Not only because, except for the PAIS Tax (which will not be renewed) and Personal Assets (the tax paid by the wealthiest is expected to bring in 22% less than this year due to the benefits approved in the fiscal package), the overall tax burden will increase. In particular, the doubling of retention revenues from one year to the next raised many suspicions.

A report from the consulting firm Epyca, led by Martín Kalos, noted: “The largest increases are expected to occur in the monotributo (which would triple from one year to the next), fuels (155% increase), and export duties (which would double). This last figure is curious: with increases of 23% in the official exchange rate on average and 9% in the value of exports of goods and services, why would export duty collections double?”

Outlier highlighted the same “inconsistency” and noted that “something similar happens with import tariffs, as with a 15% increase in the values of imports and an 18% adjustment in the official exchange rate, a 50% higher nominal collection is projected.”

The government claims that the unusual jump in export duties is due to factors beyond the projected macro variables. “The change in the payment deadlines for export duties and the soybean dollar resulted in a low comparison base for export duty collections in 2024, given the higher payments in 2023. This affects the year-on-year variation projected for 2025,” explained Martín Vauthier, advisor to Luis Caputo and official at BICE.

One interpretation circulating among economists is that the government aims to endorse the budget with a fiscal rule of zero deficit, but without establishing a clear roadmap for how this will be achieved. Outlier summarized it thus: “The Milei administration shows that it is neither willing nor interested in engaging in that discussion, thereby ensuring considerable discretion in the matter. Probably because it knows that many decisions will be made on the fly, like this year.”